Blockchain & Tokenization

“What separates the wealthy from the rest of us is in the opportunities made available to them, opportunities that aren’t readily available to the majority.”

Tokenization is most broadly defined as the representation of a particular asset, such as equity or bonds, through the issuance of tokens representing fractional shares of the underlying asset. Like a coupon redeemable for an item, a token can represent a share of any tradeable asset, such as equity, debt, real estate, commodities, and more. These tokens are issued on a blockchain or distributed ledger.

Tokenization is a developing area in the financial industry that enables investment in the form of digital tokens backed by real-world securities or assets. At the core of tokenization is blockchain technology, a type of distributed ledger which secures identical copies of data across a network of authorized stakeholders.

Tokenization unlocks liquidity by enabling fractional ownership and lowering the barriers to entry for investment in illiquid assets. Blockchain technology helps to streamline processes by allowing separate stakeholders to have secure access to the same copy of data, which cannot be altered without validation from other stakeholders.

Benefits of Tokenization

Fractionalization - Fractional ownership allows the interests in an asset to be shared among a wide pool of investors. Additionally, programmable securities enable flexible share classes and widely customizable fee structures, at a low operational cost.

Customizability – Tokenization enables exposure to individual assets. Thus, portfolios may be customized down to individual loans, buildings or even units.

Liquidity - Tokenization enables liquidity (frequently delivering a 5.0% - 20.0% premium, as compared to illiquid securities) by increasing the pool of potential investors, including potentially unaccredited investors, and by enabling secondary market trading.

Automation - Smart contracts are programs on the blockchain that facilitate the automation of processes such as compliance checks, KYC, and post-issuance matters including settlement and dividend distribution.

Cost Savings - The tokenization process can significantly reduce the administrative costs of owning an asset. Using built-in smart contracts, periodic administrative actions such as quarterly reporting or income distribution can also be automated, reducing administrative and compliance costs. Additionally, the use of DLT could expedite and condense trade clearing and settlement to nearly real-time, reducing counterparty risks and freeing up collateral, potentially producing capital efficiencies for participants in the trade. The post-trade multi-step process could be simplified and the back-office administrative burden lowered significantly.

Settlement Time - A typical timeline for a commercial property transaction can range from 6 to 24 months, and the transaction fees range from 1.0% - 3.0% of asset value. Transactions in tokenized products can be settled rapidly, potentially enabling a liquid marketplace for sizable commercial assets, or fractions thereof.

Data Transparency – Secure and transparent recordkeeping of alternative investments on a distributed ledger should increase transparency, enabling the systematic linkage of assets or market sub-segments to underlying value drivers.

Structured Products - Real-time transparency into asset performance should enable the synthesis of novel and valuable financial instruments or derivatives, used to systematically hedge risks or to make speculative investments.

Leverage – A more liquid and transparent market coupled with recent innovations from Decentralized Finance (“DeFi”), which seeks to use blockchain to disintermediate costly components of the traditional financial value chain, should enable better pricing and greater leverage.

Novel Applications – The aforementioned improvements over traditional real estate markets could enable a host of novel financial products and applications. In residential real estate in particular, a significant obstacle to homeownership for many young families is the prohibitive down payment. With tokenization, real estate companies could enable ownership gradually purchased by the tenant, on a progressive, fractional basis.

Token Types

Generally speaking, crypto-assets are broken down into multiple sub-categories:

Utility Tokens - Intended to provide access digitally to an application, services or resources available on a distributed ledger and that are accepted only by the issuer of that token to grant access to such application, services or resources available.

Asset-Referenced Tokens “Security Tokens” - Used as a means of exchange and to maintain a stable value by referring to the value of several fiat currencies, one or several commodities or one or several crypto-assets, or a combination of such assets. Tokenized versions of existing securities that have been previously issued by conventional methods (traditional share certificates), and aim to bring these assets onto the secondary on-chain market in digital form. Related, Security Token Offerings(“STOs”) have been marketed as a more “regulatory-compliant” successor of Initial Coin Offerings (“ICOs”) aiming to raise capital. Regulations applying to the offering and throughout the security lifecycle are digitally represented on the blockchain through programmable enforcement of ownership and trading restrictions, for instance (‘programmable securities’).

Cryptocurrencies (“Exchange Tokens” or “Payment Tokens”) - Used as a means of exchange and maintain a stable value by being denominated in (units of) a fiat currency.

Non-Fungible Tokens (“NFTs”) - Today the most common application of tokens that exist on DLT /Blockchains are tokens that are fungible of nature, like cryptocurrencies or ingots of gold. Fungible means that each unit of a good or commodity is interchangeable with any other unit. So, for example, one ounce of gold is interchangeable with any other kilo of ounce gold. Dissimilarly, NFTs represent assets that are by definition unique, irreplaceable and non-interchangeable. The attributes represented by NFTs can vary, comprising only unique serial numbers or more dynamic information like location, size etc. Early examples of products represented NFTs are physical items like bottles of wine, jewelry or art. Real estate is a particularly good example of a real-world asset that can be represented using NFTs as there are no two parcels that are the same or have the same address. Accordingly, direct ownership of land could be represented on an NFT

Tokenized Securities

Tokenized securities could be seen as a form of cryptography-enabled dematerialized securities that are based and recorded on a decentralized ledger, instead of electronic book-entries in securities registries of central securities depositories.

The decentralization of tokenized securities, coupled with the ability to automatically transact and settle without trusted intermediaries, maybe where most of the disruptive potential of tokenization lies. Tokenized securities eliminate the need for the use of intermediaries or proxies in the distribution of dividends or votes, giving investors full control of the equity they own.

Tokenization vs Asset-Backed Securitization

An easy way to understand the tokenization of assets that exist in the off-chain world is to use the parallel of a DLT-based asset-backed securitization. In the same way that securitization as a structured finance technique pools assets together and sells securities carrying claims on the rights (cash flows) backed by the pool of assets, tokenization of a real estate portfolio pools together real estate assets and represents the rights attached to such portfolio through tokens.

As tokens are in most cases digital representations of securities, tokenization could be considered as a proxy for asset-backed securitization on the blockchain. Through both processes, illiquid financial assets are converted into liquid marketable securities, funded by and tradable in the capital markets.

Some of the main differences between tokenization and securitization include the following:

Bundling is not necessarily the norm in tokenization

The securities being ring-fenced by originators in securitization, is not the case in tokenization

In securitization there can be credit enhancement while in tokenization the security’s/token’s credit quality can never be higher than that of the underlying asset.

Setting up a structured product is expensive, and these investments are typically buy-and-hold investments with high minimum tickets for investors. In contrast, the possibility of fractionalization for tokens enables small minimum investments.

Based on the above parallel, lessons learned in securitization markets should be considered in tokenization markets. These include special attention to the following:

Transparency of collateral

Legal clarity of token holder claims on income streams produced by the assets

Investor protection issues

Duties of asset pool managers

Incentives produced by originate-to-distribute business models

The risks specific to the offering of such products to individual investors.

Tokenized Securities vs. Tokenized Assets

Security tokenization is a subset of asset tokenization. Namely, all securities are assets but not all assets are securities. For example, tokenization of an asset such as a land title is a tokenized asset, as opposed to the tokenization of an equity or debt share.

Tokenized Securities vs Tokenized Securities

Security Tokens are blockchain-native tokens but do not exist outside of the blockchain. In contrast, Tokenized Securities are blockchain-embedded representations of real-world securities. Both security tokens and tokenized securities can confer benefits over traditional means of representing securities, such as on paper, or digitally in siloed databases. However, they differ largely in the type of legal and regulatory frameworks they may require to achieve impactful adoption.

Real Estate Tokenization Considerations & Process

Security Tokens for Real Assets

Security Tokens are regulated digital assets and create the ability to fractionalize large, expensive and illiquid commercial real estate investments into smaller pieces for more investment options. Security tokens are typically issued by an entity, corporate or an individual, and provide the token holder specified rights such as ownership, repayment of a specific sum of money, or entitlement to a share in future profits.

Generally speaking, a token that represents an ownership interest in, or carries an entitlement to receive income, dividends or revenue from, a real estate asset will likely be considered a “security”. However, this is not necessarily a straightforward determination as a token may carry rights or features from more than one category, or a token may have rights or features which change over time. Depending on the exact features, functions, characteristics and rights of a token, it may also be categorized as one or more other regulated instruments, including but not limited to: futures contracts, stored value facilities, insurance products, derivatives, structured products, commodities, e-money, loans, deposits, or bonds.

Accordingly, the legal and regulatory requirements and restrictions for the offer, distribution, holding, trading and management of security tokens may change in the future. This may result in uncertainty for both issuers of and investors in security tokens alike, which may impair adoption and secondary market liquidity.

Tokenized Securities Issuance

Depending on the regulatory jurisdiction, tokenized securities can be either directly issued on the blockchain or issued as conventional securities that are tokenized at a second stage. Direct issuance on DLTs is more straightforward for bonds, given that these are ‘bearer’ assets on which no ownership information is recorded and whose possession accords ownership, but this will ultimately depend on the jurisdiction.

Direct issuance of equities, as registered securities, is more cumbersome; the majority of current applications of equity tokenization involve the digital representation of the rights to a share. Changes in corporate legislation would be required for equity tokens issued on DLTs to be recognized as such and not as the digital representation of share certificates.

The State of Delaware in the United States has updated its General Corporation Law to allow any company to issue equity in the form of a token and for tokenized stock or share to be legally admissible as evidence of ownership (Delaware State Senate, 2017).

Regulatory Considerations: Security Tokens vs Cryptocurrencies

Unlike traditional asset classes, the novel nature of security tokens means that the law and regulations in this area are not settled nor have they been tested by courts and regulatory authorities. Although some guidance has been issued by various regulatory authorities around the world in relation to security tokens, it is likely that new developments and changes in the laws and regulations will be introduced as the technology is increasingly embraced and the market continues to develop.

Nonetheless, the SEC has taken an interest in digital assets and sought to clarify when their sale meets the definition of an investment contract. The SEC, utilizes what is referred to as the “Howey Test” to determine whether a transaction qualifies as an “investment contract” and is therefore considered a security and subject to disclosure and registration requirements under the Securities Acts of 1933 and 1934. The SEC’s consideration of the Howey Test in the context of digital assets follows:

An Investment of Money…

In a Common Enterprise…

With the Reasonable Expectation of Profits…

To be Derived from Efforts of Others.

According to the SEC, the "investment of money" test is easily satisfied with the sale of digital assets because fiat money or other digitals assets are being exchanged. In most cases, whether a digital asset qualifies as an investment contract largely turns on whether there is an "expectation of profit to be derived from the efforts of others." For example, the purchasers of a digital asset may be relying on the efforts of others if they depend on the project's backers to develop and maintain the digital network (especially in the early stages), rather than these tasks being performed by a dispersed community of unaffiliated users. The test is also met if the project's backers take steps to support the price of the digital asset, such as by creating scarcity through token burning. Another way the "efforts of others" test is met is if the project's backers continue to act in a managerial role.

For a comprehensive analysis by the SEC please reference the following publications:

https://www.sec.gov/corpfin/framework-investment-contract-analysis-digital-assets

Additional relevant regulatory bodies currently involved in digital asset regulation include the following:

CFTC

FinCEN

IRS

IOSCO

COSRA

FATF

Regulatory Considerations: Why Is Bitcoin Not a Security (Token)?

In June 2018, the former Chair of the SEC, Jay Clayton, clarified the bitcoin is not a security: "Cryptocurrencies: These are replacements for sovereign currencies, replace the dollar, the euro, the yen with bitcoin. That type of currency is not a security," said Clayton.

Regulatory Considerations: Investor Data Privacy

Security tokens typically fall within the scope of existing securities regulations, even in jurisdictions where cryptocurrencies are unregulated or banned, such that investors in security tokens may be afforded better protections and rights than investors in cryptocurrencies. As a consequence, in the context of security tokens, which may be listed on an exchange for secondary trading, the disclosure of commercially sensitive information to a wider range of potential investors would likely be necessary to facilitate investments and transactions.

The balance between data transparency enabled by blockchain technology and information privacy required in financial transactions will be an important area of future development. One manner in which data privacy on public blockchains may be protected is through novel protocols such as Zero-Knowledge Proof (“ZKP”), where one party can verify their knowledge of certain data to a counterparty without revealing what the data is.

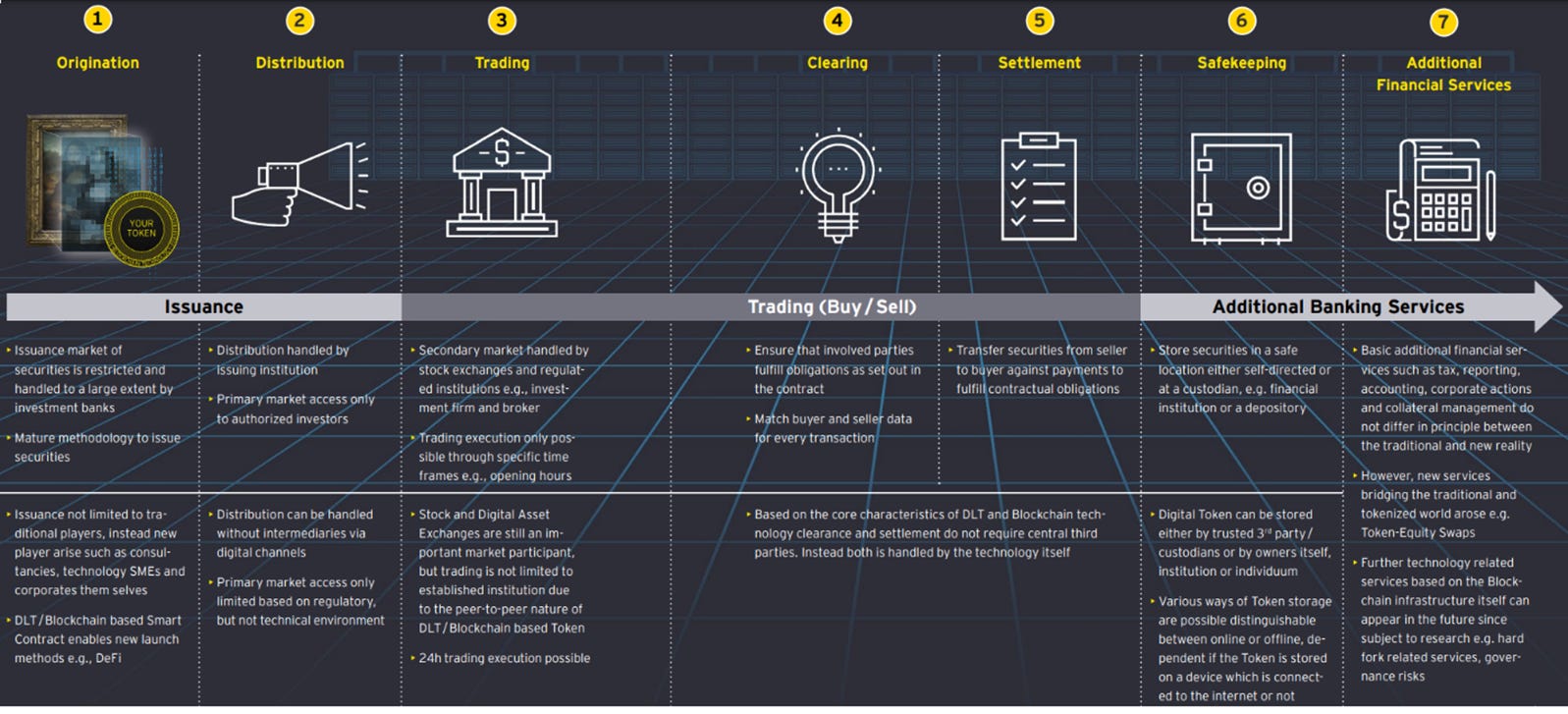

Security Token Issuance Process

The following are visual depictions of the process for issuing Security Tokens

Security Token Issuance: Process Participants

The following are the key entities involved in the process of issuing new security tokens:

Issuer - The entity that issues the tokenized security.

Digital Advisor / Underwriter / Manager - The professional advisor that assists with the offer structuring and manages the offering for the issuer. The advisor’s scope will need to be broader than in a traditional role as they will also need to provide advice in relation to other factors, including technology/blockchain selection and digital asset exchange availability and preferences. The breadth of the role means that there may need to be more than one advisor. Underwriting of tokenized securities is not yet commonly provided. However, as the market develops and more established financial institutions become involved, it is possible that underwriting will develop in the same way that it is essential to many traditional fundraising options. A manager may be able to assist in ensuring that the tokenized security is issued and administrated on an ongoing basis in a compliant and efficient manner. An increasing number of tokenization platforms and service providers are acquiring licenses themselves to provide regulated functions such as advice, custody, agency services etc.

Technology Provider - The specialist that provides the blockchain platform technology and creates the token/smart contract on the platform. These may be professional firms that are hired for a particular transaction by the issuer. Other issuers who are more involved in the digital market may prefer to build this capability in-house.

Technology Auditors - The specialist to audit the blockchain platform and any smart contracts and assess cybersecurity risk. We expect that as the market becomes more established, a more formal process of audit and verification of the underlying technology will be expected by investors and regulators.

Accountants - To provide tax and accounting analysis as necessary. This will involve advice and opinions on the classification of the tokenized securities and may also evolve to include support for advisors, such as the provision of comfort letters and opinions (as is the case in the traditional securities market).

Lawyers - Lawyers with the necessary skills to work on deal structuring, regulatory analysis, documentation and compliance. This may also involve opinions.

Custodian / Trustee - Custodians and Trustees will still be required for certain tokenized security structures.

Central Securities Depositories (CSDs) - Tokenized securities with multiple parties recording ownership on a single register will call into question many of the current operational requirements that are driven by regulations (e.g. physical certification of bonds, and the requirement for securities to be recorded on a register by a 3rd party registrar, depending on the market). While the nominee and registrar could be replaced by blockchain and smart contracts, in many cases, law and/or regulation will need to change to allow for that to happen, so the process must be very clearly mapped out to ensure it can work.

Security Token Issuance: Required Documents

Token Purchase / Underwriting Agreement - The purchase agreement or underwriting agreement will largely follow the approach used for traditional securities. However, the forms will differ depending on the particular transaction. It may be a direct subscription with the end purchasers or a subscription/underwriting agreement similar to the traditional capital markets approach:

Direct Purchase Agreement - Direct purchase agreements entered into with each purchaser of the tokenized securities. This could include different versions for pre-sale purchasers, cornerstone investors and a form that public investors would sign at the time of a public offering. It may also be made available in digital form only and signed electronically through the platform portal/website.

Manager Subscription Agreement - Similar to a traditional subscription agreement, it sets out the terms on which the issuer agrees to issue the tokenized securities, for which the managers agree to subscribe. Managers will need to consider whether the issue of tokenized securities is to be hard underwritten and whether syndication of the offering is required. In this situation, managers would need to have the ability to hold the tokenized securities in the situation where the underwriting obligation is triggered.

Tokenized Security Terms - Similar to a document that creates a traditional security, such as a Memorandum and Articles, Deed of Covenant or Trust Deed, this document would constitute the tokenized securities to be issued. Although digital assets are created through the issue of tokens on the relevant blockchain, a distinct enacting/enabling deed or set of terms can provide greater clarity and legal certainty for the enforceability of the tokenized securities. This document should set out the terms and conditions of the tokenized security, including any rights and/or obligations built into the instrument. It would also need to confirm the link between the token and the asset it represents. A consideration in preparing this document is the extent to which its contents may be expressed or incorporated in the smart contract, as well as the legal relationship between the smart contract of the tokenized security and this document. This document can be integrated into the one in the row above as part of issuance but should be capable of standing alone.

Custody Deed - There may still need to be a separate custody arrangement established if traditional assets back the tokenized security, or if any other assets will be held in custody (such as distributions). This would follow a traditional form custody agreement with adaptations as required.

Technology Implementation / Support Agreement - If a third party is providing the blockchain and platform technology, this agreement will set out the agreed scope of work and split of liability in the case of technology failure. It may also deal with ongoing support and coverage. If third parties, such as arrangers or market participants, need access to a digital platform to assist with market operations, liquidity etc, this agreement may also deal with the technical aspects of integration.

Offering Documents - The offering document should provide a description of the terms of the tokenized securities and material information on the issuer, including financial information if available. Issuers should consider robust risk disclosure, in particular in relation to the new technology and uncertain nature of some of the features of tokenized securities. Even if the disclosure is not required under relevant regulations, clear disclosure to investors can help reduce the risk for the issuer and managers.

Security Token Issuance: Possible Alternative - NFTs for Real Assets

In many respects, real assets are no different than collectibles or works of art. Because they occupy a static, physical location, they may be considered genuinely unique, relative to all other assets of the same category. For this reason, it is possible to issue NFT’s for any given real asset, or its subcomponents. For example, NFT’s could represent entire properties, sub-divisions of a property, floors in a building, units on a floor or rooms in a hotel.

Sources

https://realio.fund/wp-content/uploads/2021/01/rst-pitch-deck.pdf